In the war of convergence, the eco-system is expected to favour the species which collaborates and coordinates the most with other stakeholders out there. So being "OPEN" is "IN"! Open Source and Crowd Sourcing are the new buzzwords of the new era. The case in point is the spawning of Application stores after Apple has successfully used it as SaaS differentiator versus other players in the smartphone space. The other case in point is the coming of age of crowd sourced platforms such as Digg and Twitter. Even while Convergence of Internet and mobile services is a event in process, the technology frontier has now moved to Cloud computing (instead of desktop computing and legacy systems.)

The cloud eco-system, is effectively using the following as service based business models.

IaaS: Infrastructure as a Service

PaaS: Platform as a Service

Saas: Software as a Service.

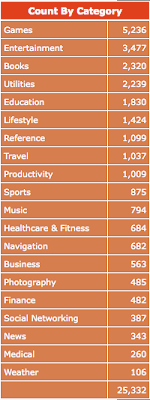

Refer to the slide below for a snap shot of the service models that are being hosted by the cloud.

I shall not be probing into the depths of each of these cloud hosted services. Instead, we will try to draw the Telecom industry equivalent of Cloud Services --> Lets call this Telco 2.0 eco system (and services).

In as far as IaaS is concerned, Telco's are sharing the infrastructure and keeping the costs under control. This gives them the ability to focus their efforts in building greater foot prints, bigger advertising budgets and larger promotions (which on the other hand is commoditizing the core product.) Also IaaS means the SME network and voice solutions being provided. The central idea in here is that money made through the IaaS route is not being used for any significant innovation efforts.

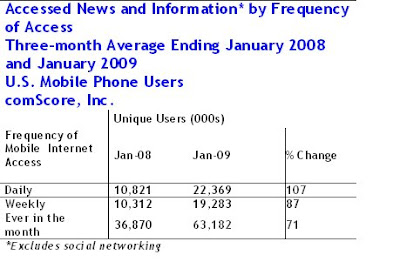

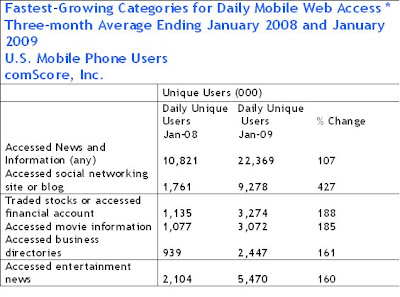

As far as SaaS and PaaS is concerned, Telco's have little and no control on this aspect of the eco system. The control rests either with the internet/web 2.0 pioneers -->Google, Yahoo, FaceBook, Twitter etc or lies with the OS system holder --> Nokia, Apple, Google, Palm, Microsoft, RIM etc. The operator makes money through the usage and just that. It exercises no control over Content, Consumer or the Device. (For Telco Carriers (At&T, Sprint , Verizon etc) there is a point here, since they have the choice of devices on their network. Hence there is some amount of co-creation.) However there are ominous signs that the iPhone style model is winning, i.e. Telco's are being used as a transaction point in the retail channel but all the real value is ending up outside the Telco eco-system. A recent release by AT&T and Canadian Rogers have indicated increase of data usage on their networks through the introduction of iPhone and a subsequent increase in data ARPU. However, the iPhone cost subsidy doesnot allow higher usage of data translate into direct profits for these carriers.

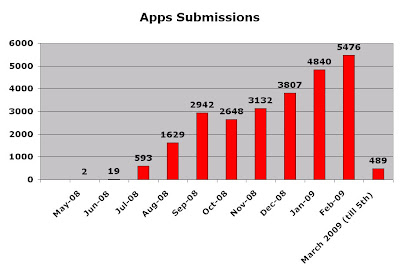

Tabulated below is AT&T and Rogers numbers for the year 2008.

With voice moving towards zero tarriffs (VoiP: Skype and Google Voice anyone?) and mobile broadband commoditizing fast, the margins of the operators who have been the lords of the Telecom eco-system is under huge pressure. Thus the operator is at a threat of being used simply to transfer bytes to and from the customer’s device and not being able to increase their position or add any additional services beyond simple network operations. Thats the dumb pipe. (The term basically stems from the internet where ISPs managed to botch their position and now provide nothing but connection and bandwidth.). Operators can increase charges and higher percentages in the revenue generated by the content providers for using the operator pipeline. However, this is unsustainable because it results in high prices for end users, and consumers being deterred from accessing mobile content on a wider scale.

Endnote: With services getting polarized towards content providers and OS makers and device manufacturers, the Operators will need to differentiate thier offerings and must innovate on their services to maintain their relevance in the Telecom eco-system.

A report by Juniper Research, examines the three main scenarios facing the operators and the sector as a whole – the 'dumb pipe', 'smart pipe' and 'on-portal' routes. One single scenario will not win out, since different business and revenue models have to co-exist in the mobile content market.Players will adopt multiple approaches that best fit their markets. Crucially, if MNOs are to benefit financially, they need to move away from their dumb pipe roots to the smart pipe model, though they will clash with the content providers which already dominate the smart pipe.

The report predicts that under the smart pipe model, MNOs will not see their share of the overall mobile content market rise appreciably, but revenue will rise in value by 125 per cent over the 2008 to 2013 period.Meanwhile under the on-portal scenario, content providers will see their share of the market rise from 54 per cent in 2008 to 68 per cent by 2013, providing they can secure more attractive terms from MNOs.The report also concludes that various players can find a compromise and concludes that if MNOs can change their focus from the traditional average revenue-per-user mindset, to instead concentrating on value creation and support for their partners, they can swiftly make the change to a more beneficial scenario for everyone. In effect, it advocates moving away from the existing mindset to a more collaborative view of the eco-system.

References:

mobile analyst firm Juniper Research's recent Mobile Content Strategies & Business Models: Scenarios & Forecasts 2008-2013 report

.jpg)

Canadian based Telco Rogers, has also reported 36% boost to its data revenues because of iPhone in its portfolio. iPhone now contributes 33% to Roger's Smartphone sales. (

Canadian based Telco Rogers, has also reported 36% boost to its data revenues because of iPhone in its portfolio. iPhone now contributes 33% to Roger's Smartphone sales. (

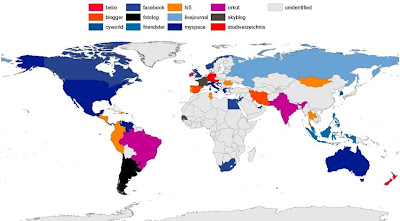

While this schematic is a little old (June 2007) it gives a pretty clear picture of the dominance of social networking websites in the world. The Dark Blue (Facebook) features prominently in Canada, Australia, South Africa, Egypt, UK, Scandinavia, South Korea, Italy and parts of Eurasia. Since then the spread of the Blue would have increased by a factor of 3.5 and would porominently feature the whole North American continent. Facebook's march to 200 million users earnestly began in January 2008, when it made translation tools available to the international user. Today more than 70% Facebook users are outside USA and most of them read it in their native language.

While this schematic is a little old (June 2007) it gives a pretty clear picture of the dominance of social networking websites in the world. The Dark Blue (Facebook) features prominently in Canada, Australia, South Africa, Egypt, UK, Scandinavia, South Korea, Italy and parts of Eurasia. Since then the spread of the Blue would have increased by a factor of 3.5 and would porominently feature the whole North American continent. Facebook's march to 200 million users earnestly began in January 2008, when it made translation tools available to the international user. Today more than 70% Facebook users are outside USA and most of them read it in their native language. In 2005, Mark Zuckerberg had outlined his vision for Facebook to be an online "social utility" tool which would mean a global digital phone book which users would use to locate people on the web. In strictest terms the vision has not changed very hugely except that instead of Phone book (assisting medium), facebook intends to usurp the position of the phone itself. He dreams of Facbook to be the central portal for communication, work and pleasure. It also becomes the central place where users organize parties, store pictures, find jobs, watch videos and play games. eventually , Facebook will become an online passkey to gain access to websites and online forums that require personal identification. In other words, Facebook will be the place where people will live their digital lives in the internet of the future.

In 2005, Mark Zuckerberg had outlined his vision for Facebook to be an online "social utility" tool which would mean a global digital phone book which users would use to locate people on the web. In strictest terms the vision has not changed very hugely except that instead of Phone book (assisting medium), facebook intends to usurp the position of the phone itself. He dreams of Facbook to be the central portal for communication, work and pleasure. It also becomes the central place where users organize parties, store pictures, find jobs, watch videos and play games. eventually , Facebook will become an online passkey to gain access to websites and online forums that require personal identification. In other words, Facebook will be the place where people will live their digital lives in the internet of the future.